MEXICO BARRIERS: NOBEL STUDY REVEALS PATH

Researchers Win Nobel Prize in Economics for Work on Poverty in Mexico.

2024 Nobel Prize in Economics Awarded for Research on Wealth Inequality Between Nations.

Daron Acemoglu, Simon Johnson, and James A. Robinson received the Nobel Prize in Economics for their study on how institutions impact prosperity. "Reducing the enormous income disparities between countries is one of the greatest challenges of our time. The awardees have demonstrated the importance of social institutions in achieving this," stated Jakob Svensson, chairman of the Economic Sciences Prize Committee.

According to the committee, the three laureates have shown the significance of social institutions for the prosperity of nations, highlighting that societies with weak rule of law and institutions that tend to exploit the population do not generate growth or changes that lead to improvement. El Sol de Mexico

2024 Nobel Prize in Economics Awarded to Authors of a Study in Mexico.

The jury emphasized that one of the most pressing current challenges is reducing global inequality, and that the work of the three economists highlights the relevance of inclusive institutions in sustainable economic growth. These institutions not only improve the quality of life for individuals but also foster a democratic and stable environment, in contrast to extractive institutions, which typically benefit only a small elite. Despite historical limitations, the study suggests that change is possible. When countries succeed in establishing the rule of law and democratizing, the social and economic benefits can be significant and long-lasting.

"Carlos Slim: Key Figure in Mexico's Inequality, Say 2024 Nobel Laureates".

Daron Acemoglu and James Robinson emphasize that Slim's wealth was not built on innovation, as seen in other economic contexts, but through exclusive contracts. According to the economists and Nobel laureates, the philanthropist did not earn his wealth through innovation, but rather through the strategic acquisition of key companies, notably the purchase of Telmex, the state telecommunications company privatized during the administration of former President Carlos Salinas de Gortari.

According to the economists, Slim's offer was not the best; however, the consortium led by the magnate, Grupo Carso, won the auction. One of the most critical aspects of the purchase was that Slim did not pay for the shares upfront; instead, he used the dividends generated by Telmex itself to cover the acquisition cost. What was once a public monopoly had turned into Slim's private monopoly and became highly profitable. La Silla Rota

Reform to Reassert Government Control of Railways Advances in the Senate.

The Constitutional Points, Legislative Studies, and Communications and Transportation committees approved the reform to Article 28 of the Constitution, allowing the federal government to once again provide passenger and cargo transport services.

The bill, which will be presented to the full Senate, was approved unanimously. The initiative initially approved by the Chamber of Deputies proposes an amendment to Article 28 of the Constitution, stating that railway services provided by the government will not be considered a monopoly.

Additionally, it adds a paragraph to Article 28, which will read: “The Mexican State reclaims the right to use railway tracks to provide passenger transport services. To this end, the Federal Executive may grant assignments to public companies or concessions to private entities.” La Silla Rota

Starlink Is a Viable Business

Although Elon Musk's Tesla investment remains on hold, Mexico continues to be a profitable venture for the entrepreneur. Starlink, Musk's satellite internet service, has become the sixth largest internet provider by customer count in the country, making it the second most important market for the company in Latin America, following Brazil. However, it is not far behind, with a difference of less than 64,000 fixed satellite internet accesses. El Financiero

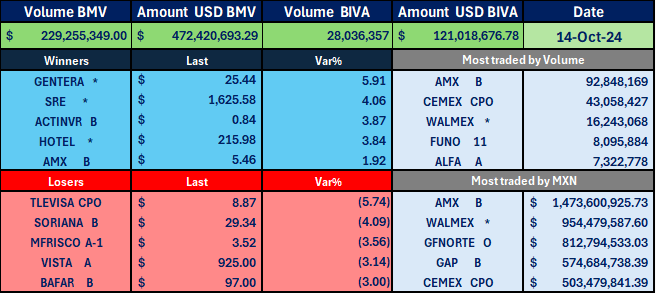

VECTOR SALES AND TRADING DESK

MEXICAN BANKS: GENTERA +5.91%, GFNORTEO -2.56% on August CNBV data.

Data published by the National Banking and Securities Commission, as of August, the total credit portfolio of the banking system grew by 11.8% year-on-year. 20 banking institutions reported a greater credit portfolio growth than the system in August, among which Inbursa (+39.0% year-on-year), Compartamos (+35.6% year-on-year), Invex (+26.3% year-on-year), BBVA Mexico (+14.0% year-on-year), and Banregio (+12.5% year-on-year) stand out. Although Banorte grew below the industry average (+9.9% year-on-year), it is within the range stipulated in the results guide for the current year. During the same period, the average reference rate has decreased by 50 basis points, as a result of the initiation of an expansive monetary policy. Of the 50 banking institutions analyzed, the ten largest according to the credit portfolio represent 88.6% of the total. In detail, these institutions are: BBVA Mexico (25.1%), Banorte (14.7%), Santander (12.2%), Banamex (8.4%), Scotiabank (7.2%), HSBC (6.8%), Inbursa (6.1%), Banco del Bajío (3.4%), Banco Azteca (2.5%), and Banregio (2.3%).

GMXT*: Derailment Creates New Setback for Grain Exports Between the U.S. and Mexico.

A derailment has disrupted rail traffic in Eagle Pass, leading Ferromex and Union Pacific to suspend the issuance of permits for grain shipments. This situation significantly impacts exports between both countries, creating a new challenge for producers and traders. The railway consortium Ferromex and the American company Union Pacific Corp announced that they have stopped issuing permits for certain grain shipments moving through Eagle Pass, Texas, following a recent train derailment in Mexico that closed the track.

Ferromex, part of Grupo México Transportes and operating the largest railway in the country, notified Union Pacific about the derailment on Saturday, according to the American firm. FXE told Reuters that the track was closed for up to 15 hours.

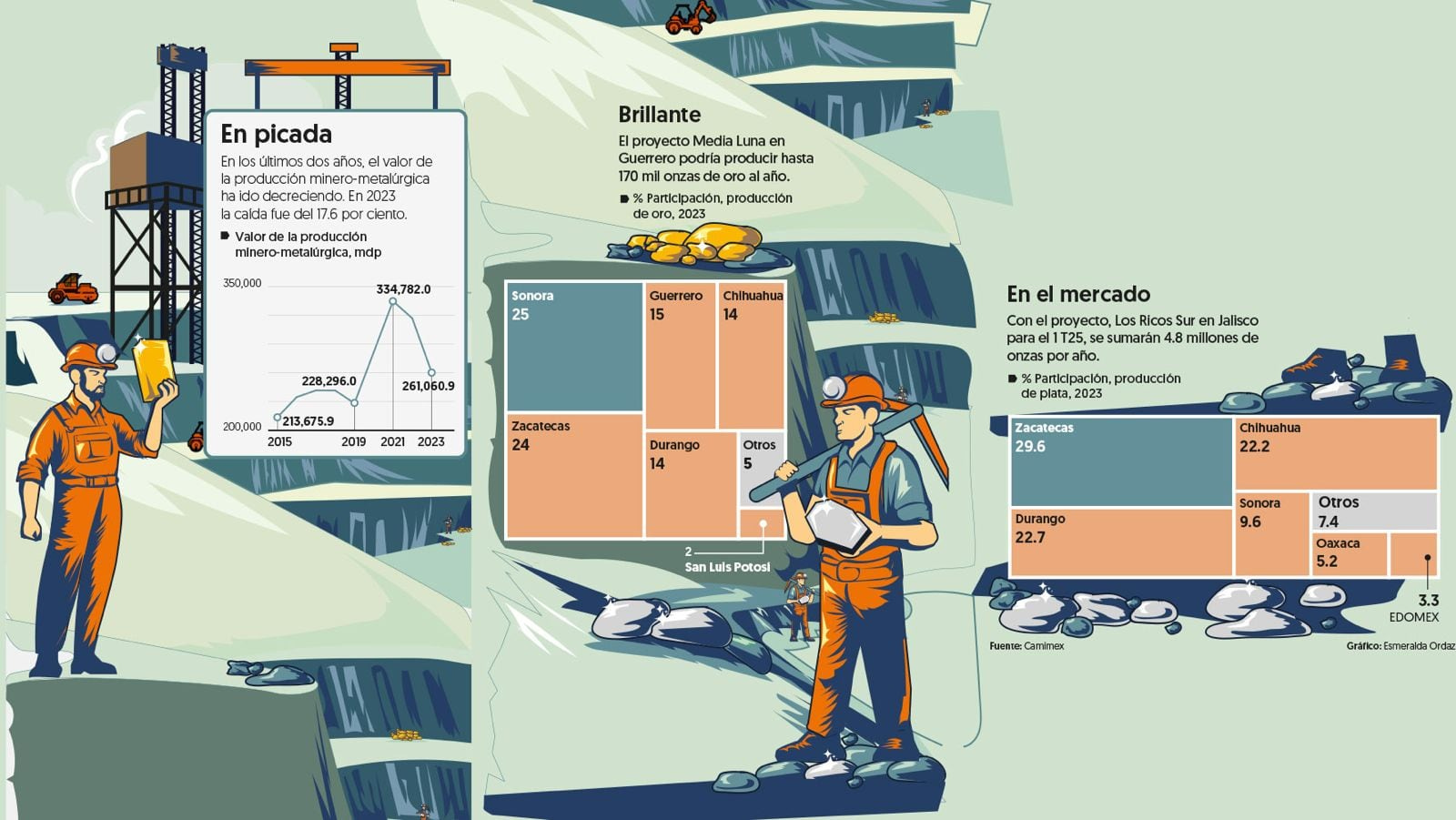

PE&OLES*: Seven gold and silver mines will begin operations. Media Luna is the largest gold project, and operations are expected to start in the first months of 2025.

Mexico will have four new active gold mines in the next six months that will produce 306,400 ounces annually, and three silver mines that will yield 10.6 million ounces of silver per year. This might seem like positive news given that the projects total investments of $1.1745 billion, but the reality is that the industry is tense, as the start of all these could place the sector back under the scrutiny of President Claudia Sheinbaum, who has expressed the intention to prohibit open-pit mining.

GMEXICOB: The Congress will revisit the discussion on the reform to prohibit open-pit mining in 2025. Although it is not a priority on the current agenda and is not expected to be discussed this year, the topic is anticipated to gain relevance due to the opening of seven gold and silver mining projects, as well as four copper projects that will begin operations in the next six months, including one from Grupo México, led by Germán Larrea.

Additionally, the Supreme Court of Justice of the Nation (SCJN) granted a protection order against the mining law reform promoted by former President López Obrador and approved in 2023, which protects the concession scheme under which the company operates.

CEMEXCPO: Stock lost -2.4%.

Construction Sector Unexpectedly Pulls Down Mexico's Industrial Activity in August. Data released Friday October 11th.

Mexico's industrial activity broke a rising streak in August, recording its worst performance for that month in six years, largely due to poor construction figures overshadowing gains in other sectors.

In August, the country's industrial production experienced a seasonally adjusted monthly contraction of 0.5%, ending three consecutive months of growth, according to the National Institute of Statistics and Geography.

This decline marked the sharpest drop for August since 2018, causing the industrial production index to fall to 104.1 units, or 0.7% below the highest historical level reached nearly a year ago.

The results also fell short of expectations from our estimate, monthly increase of 0.3%.

We believe industrial activity is showing increasing signs of weakness, highlighted by the surprising drop in construction and marked stagnation in manufacturing. It's worth noting that, with these results, the IMAI has accumulated five months of growth below 1% annually, emphasizing the downward trend observed since October 2023.

Given this context, the 2025 Economic Package will be crucial in terms of physical investment spending, especially since the previous administration ended with a decline in this type of expenditure—something not seen in at least the last four administrations.

GFNORTEO: Moody's upgraded Banorte's long-term deposit ratings from 'Baa2' to 'Baa1' and its long-term counterparty risk rating from 'Baa1' to 'A3'. Moreover, the foreign currency senior debt rating of Banorte's Cayman subsidiary was raised from 'Baa2' to 'Baa1'. The outlook for both entities was revised from positive to stable.

GICSAB: AGAIN IN DEFAULT, S&P LOWERS RATING AND ANTIQUATED PHILOSOPHY

The real estate developer and operator GICSA, led by Elías and Abraham Cababie, was downgraded by S&P on Friday due to default and the proposed restructuring with its bondholders. The determination includes a negative outlook for the issuer, indicating that its rating will soon be "SD," or selective default. Decades of GICSA placing and not paying. Part of a philosophy.

CERAMICB: Today marks the end of the public buyout offer for the remaining shares of Interceramic, which represent 0.15% of the company's share capital. The flooring and coverings company has decided to exit the stock market, but it first needs to acquire all the outstanding shares before initiating the delisting process from the Mexican Stock Exchange (BMV).

OIL: CL1. Oil drops -4% after Netanyahu Tells U.S. That Israel Will Strike Iranian Military, Not Nuclear Or Oil, Targets, Officials Say.

Israeli Prime Minister Benjamin Netanyahu has told the Biden administration he is willing to strike military rather than oil or nuclear facilities in Iran, according to two officials familiar with the matter, suggesting a more limited counterstrike aimed at preventing a full-scale war.

In the two weeks since Iran's latest missile barrage on Israel, its second direct attack in six months, the Middle East has braced for Israel's promised response, fearing the two countries' decades-long shadow war could explode into a head-on military confrontation. It comes at a politically fraught time for Washington, less than a month before the election, and President Joe Biden has said publicly he would not support an Israeli strike on nuclear-related sites.

VECTOR RESEARCH

EQUITY STRATEGY

At current prices, the Mexican stock market has partially absorbed the effects of the constitutional reforms that have been approved, particularly those aimed at the judiciary. We consider it essential to closely monitor indicators of foreign direct investment and business confidence in the coming months, and how they might negatively impact the trajectory of economic growth. However, we still see that at least in the short term, the fundamentals of the economy would remain relatively stable, and if our profit generation forecast is viable, we will see very attractive valuations due to the decrease in multiples.

Therefore, we believe that opportunities for purchases may arise in the stock market due to the appealing undervaluation levels presented by the S&P/BMV IPC. Regarding the investment strategy in Mexico, we consider it reasonable to tactically increase positions in the national market based on the valuation levels we calculate, while awaiting more information about the current government transition and the signals it will provide to investors, as well as the release of the fiscal package for 2025 and the upcoming presidential elections in the U.S. For investors with a more risk-averse profile, we continue to favor a highly selective stock-picking approach in Mexico.

With consolidated figures from the sample of issuers that make up the S&P/BMV IPC (which includes 26 covered companies and 9 with consensus estimates), we expect a 7.6% year-over-year increase in revenues for Q3 2024, an 11.8% year-over-year increase in EBITDA, and a 27.1% year-over-year growth in net income. As previously noted, the financial results of companies will show mixed exchange rate effects, where highly export-oriented sectors or those with operations outside Mexico will benefit most from their revenues denominated in USD, along with improved operating leverage that will allow them to enhance their profit margins. Consequently, we anticipate an aggregate EBITDA margin expansion of 86.8 basis points year-over-year. We also expect the net margin to expand by 133.1 basis points year-over-year, driven by foreign exchange gains from the USD appreciating against the MXN by 7.7% quarter-over-quarter in Q3 2024, applied to the net USD asset position of the companies.

It’s important to highlight the non-recurring effects in the results that affect comparability: in this regard, we made adjustments to the aggregated figures due to FEMSA's sale of its stake in Heineken, which generated MXN 40.606 billion in extraordinary gains included in Q1 2023 results. Additionally, FEMSA sold a majority stake in Envoy Solutions in the second half of last year, so we also adjusted the revenues from this business (MXN 13.467 billion) and EBITDA (MXN 931 million) to "normalize" growth.

Regarding the subset of issuers under VectorAnálisis coverage, for the group of commercial and service companies, we expect a 7.4% year-over-year increase in revenues for Q3 2024, a 12.4% year-over-year increase in EBITDA, and a 36.1% year-over-year growth in net income.

For the financial sector, with GFNORTE being the only covered company, we expect total revenues (including financial margin) to rise by 7.7% year-over-year, operating income to grow by 0.1% year-over-year, and net income to increase by 3.9% year-over-year.

In the FIBRAs sector, among covered issuers, we anticipate a 6.8% year-over-year growth in revenues, a 3.7% year-over-year increase in NOI, and a 5.4% year-over-year rise in FFO.

Regarding exchange rate trends, as mentioned earlier, the USD appreciated against the MXN by 11.0% year-over-year in average quotations (equivalent to a depreciation of the MXN against the USD of 9.9% year-over-year). The effect on results was significant, as the comparative base from the previous year is very low, due to the USD depreciating by 15.7% year-over-year against the MXN in Q3 2023. This phenomenon benefited companies with USD-denominated revenues, while positively impacting the margins of firms exposed to commodities and expenses denominated in this currency.

Concerning the closing MXN/USD exchange rate behavior, the USD appreciated by 7.7% quarter-over-quarter in Q3 2024 (equivalent to a depreciation of the MXN against the USD of 7.1% quarter-over-quarter). This benefited companies with a high composition of net monetary assets denominated in USD, which will record foreign exchange gains during Q3 2024. Conversely, companies with net liabilities denominated in USD will incur foreign exchange losses.

In terms of exchange rate volatility in significant functional currencies in South America, the currency that depreciated the most against the USD in Q3 2024 was the Argentine peso (ARS), with a depreciation of 200.5% year-over-year, resulting in very unfavorable exchange effects for companies with a presence in Argentina. The Brazilian real (BRL) also recorded a depreciation of 13.0% against the USD. To a lesser extent, the Chilean peso (CLP) showed a depreciation of 4.1% year-over-year against the USD, while the Colombian peso (COP) depreciated only 1.2% year-over-year.

The best reports we anticipate for Q3 2024, from our perspective, are those of: BOLSA, DANHOS, GRUMA, LAB, LIVEPOL, LACOMER, GMEXICO, PE&OLES, and VOLAR.

Conversely, the most negative reports we expect include: ALSEA, CHDRAUI, CUERVO, KIMBER, SORIANA, OMA, CEMEX, and ORBIA.

MEXICO CORE PORTFOLIO:

On this occasion, we are incorporating GRUMA (+3.37 p.p.) into our portfolio, with the expectation of a positive report in the results for Q3 2024. While we believe that the appeal process and the lawsuit against COFECE could generate some volatility in the stock, from our perspective, the negative impact would be limited. In the worst-case scenario, the projected timelines for divesting the plants, along with the geographical and business diversification of the issuer, would cushion any potential adverse effects on its operations in Mexico.

Additionally, we are reducing our overexposure in WALMEX (-2.86 p.p.), adjusting it to a neutral weighting relative to the benchmark. This decision is based on our expectation of a neutral report for Q3 2024, as well as the possibility that the projected number of store openings for 2025 may be lower due to potential delays in permits stemming from the change in government administration.

Furthermore, we are reducing our position in ORBIA (-0.51 p.p.) to align our exposure with that of the S&P/BMV IPC. We expect a negative report for Q3 2024. We believe that the issuer could lower its annual guidance due to ongoing weakness in some of its main businesses and markets.

FIXED INCOME STRATEGY

The local fixed income market showed a flattening dynamic with widespread increases of up to 36 basis points across the yield curve. Interest rates have risen in recent sessions following the release of economic data in the United States and comments from Federal Reserve members, which have sparked increased debate about the pace of monetary easing globally. As a result, a stronger correlation has been observed between Mbonos and U.S. Treasury bonds, amid a lack of local catalysts and investor concerns regarding expectations of a more gradual approach to rate cuts due to resilient inflation and the strength of the U.S. labor market.

In this context, the implied monetary policy expectations in Mexican market instruments have undergone significant changes, anticipating a smaller rate-cutting cycle than previously estimated.

Next week in the U.S., the publication of retail sales, industrial production, as well as employment and housing data are notable; while in Mexico, the publication of consumer confidence is expected.

In terms of long-term prospects, there is significant potential for capital gains stemming from the anticipated rate-cutting cycle of the Bank of Mexico. Therefore, maintaining exposure to Mbonos is recommended, particularly focusing on the 3 to 10-year sector. Additionally, it is tactically advised to enter the longer end of the yield curve.

VOLARA: The short-term adjustment seems to have found support at the 50-day moving average at 11.99. As long as this demand level holds, it is likely to enter a new recovery period, with initial resistance at 12.95 pesos. However, caution is advised, as the velocity indicator shows a downward trend. If the price falls below the average, it could drop to 11 before potentially starting a recovery.

INTERNATIONAL DAY

October 15 is also known as National Grouch Day celebrates the world’s favorite grouch, Oscar, from “Sesame Street.” This day invites us to embrace our inner grouch, allowing for a little complaining and irritable behavior. It reminds us that processing negative emotions is a natural part of life.